The phrase “cronyism and corruption” is not one I use lightly. It implies more than error, more than poor judgment, and more than bureaucratic inertia. It implies the misuse of public authority for private benefit. When applied to a city government, it carries a particular weight, because the system involved depends almost entirely on trust. This chapter concerns how they appear in the public record of a functioning government.

When I first started looking into it, I assumed that what I was seeing in Grosse Pointe Park’s property tax records would prove to be a misunderstanding—or a clerical anomaly that would dissolve under closer inspection. That assumption did not survive contact with the documents.

What survived instead was a pattern.

This chapter does not attempt to reproduce that pattern in full. Doing so would be both inefficient and misleading. The work required to understand it is cumulative. Individual records stand on their own. It is only when they are aligned chronologically, compared across time intervals, and examined alongside public roles and private relationships that they take on the full meaning. But the exhibits above cry “cronyism and corruption” and speak volumes!

The comprehensive analysis lives elsewhere.

I spent more than five hundred hours assembling the public records, timelines, and source documents referenced in this chapter. They are available in full, at the following website (last updated May 15, 2020 at which point in total frustration—with the message falling on deaf ears I put the effort on pause)

https://www.theokas-richner-gpp-tax-fraud.net

wait a second for the website to load

This book chapter is a narrative medium. The website exists so that readers who wish to test what I am saying—or reject it—can do so directly, using the same materials I did.

The records collected there are all public. They include property tax assessments, ownership histories, transaction timelines, public filings, and correspondence obtained through lawful requests. Every document is cited. No conclusions rely on private information, leaks, or speculation.

The website is organized to make sequence visible, because sequence is where this story lives.

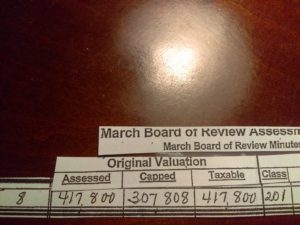

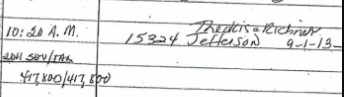

Corruption in property taxation does not usually announce itself through dramatic acts. It operates quietly, through administrative discretion exercised unevenly, through valuation changes that lack corresponding physical or market explanations, and through decisions that consistently benefit individuals who are professionally or financially adjacent to those making them.

The issue at hand —documented in detail on the site—illustrates the method. A property experienced a substantial reduction in assessed value during a period in which there was no documented deterioration, no neighborhood-wide decline, and no comparable adjustment for similarly situated properties. The change occurred through administrative channels, not public vote. Individuals who benefited from the reduction had professional relationships with city officials involved in the tax assessment decision process and in fact one was a city official at the time.

Those statements are factual. Whether they amount to corruption is a conclusion the reader is free to draw or reject. The website exists to make that judgment possible. I have reached my conclusion.

This chapter, then, is not an indictment but an allegation. It is an explanation of why an indictment—if one is to be made—must rest on documents rather than rhetoric.

Property taxation functions only because most people accept its legitimacy even when it produces outcomes they dislike. That legitimacy erodes quickly when discretion appears selective and unexplained. The conduct documented on the website and in this book chapter, taken as a whole, raises serious questions about whether that discretion was exercised in the public interest.

This website tells the story of how I came to confront those questions, what it cost, and what it revealed about the fragility of institutions that rely on trust without transparency. The website exists for readers who want to examine the underlying record themselves.

I do not ask the reader to accept my conclusions.

I ask only that, if they choose to judge, they do so with the full record in view.

The full record is available in full, at the following website (last updated May 15, 2020 at which point in total frustration—with the message falling on dear ears I put the effort on pause)

https://www.theokas-richner-gpp-tax-fraud.net

wait a second for the website to load

Beyond the alleged property-tax fraud, the website argues that Gregory Theokas’s alleged self-dealing caused the City of Grosse Pointe Park substantial additional financial losses—losses that far exceed those arising from the property-tax matter itself. Although Andrew Richner was not a city official at the time of Theokas’s self-dealing he benefitted from that self-dealing in his real estate venture with Theokas.